Bonds: What are they and how do you invest?

Bonds offer stability, interest income, and diversification. Discover how they work, how they're priced, and how to use them wisely in your portfolio.

“Stocks bring adrenaline, bonds bring calm.” For many investors, the stock market feels like a rollercoaster. Bonds are the stabilizing factor in this context: less spectacular than stocks, but essential for a balanced portfolio. In this guide, you'll discover what bonds are, how they're priced, when they yield, and how to use them practically without endless spreadsheets.

What is a bond?

A bond is simply a loan you grant to a government, company, or institution. You hand over your money and receive a fixed interest rate in return ( ) and after the term, you receive your original investment back. It's a contractual agreement, meaning bonds generally offer more security than stocks.

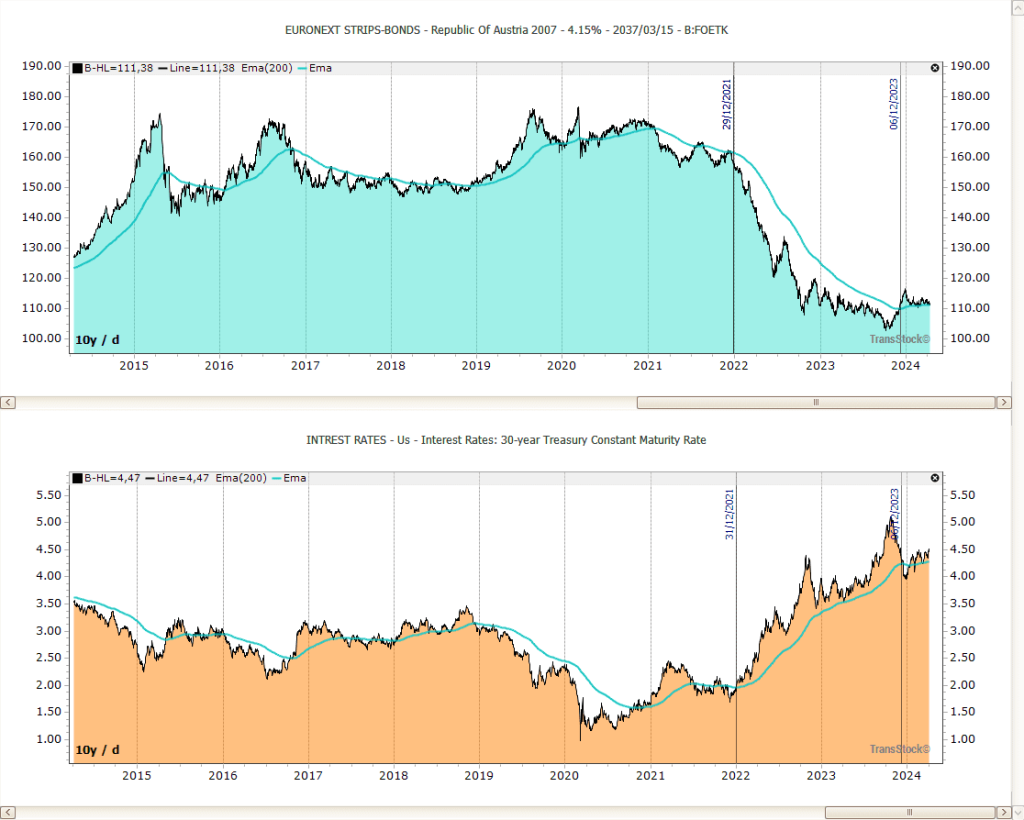

How does pricing work?

The value of bonds fluctuates depending on interest rates and creditworthiness:

- Interest rates rise → bond prices fall. New issues become more attractive, old ones decrease in value.

- Interest rates fall → bond prices rise. Your existing coupon is more attractive than the new lower interest rate.

- Credit risk: Government bonds from strong countries are safer, but pay lower interest. Corporate bonds with higher risk reward you with higher coupons.

Benefits of bonds

- Stable cash flow: coupons provide regular income.

- Rest in the wallet: Bonds dampen the volatility of stocks.

- Diversification: different maturities, regions and types limit risks.

- Preparing for retirement: Bonds provide stability as your horizon shortens.

Types of bonds

- Government bonds: issued by governments; high security, lower coupon.

- Corporate bonds: issued by companies; higher interest, more risk.

- High-yield bonds: attractive interest rate but with higher default risk.

- Inflation-linked bonds: protect your purchasing power when prices rise.

Why bonds in your mix?

- Stable cash flows: Predictable coupon payments are useful towards retirement or for periodic withdrawals.

- Shock absorber: They dampen volatility when stocks move sharply.

- Goal oriented: with terms (duration) you align your interest rate risk with your horizon.

Strategies: How to tackle it

- Bond ladder: Spread the maturity dates (1, 3, 5, 7, and 10 years). When one matures, you reinvest at the then-current interest rate.

- Funds/ETFs: Broad diversification across publishers and sectors; less work, but higher fund/ETF costs.

- Credit quality: Determine your mix between investment grade and high yield, in line with risk comfort.

- Currency & Inflation: track exchange rate and inflation risk (consider TIPS/ILB-like products).

Do you want to sell your bonds? specific see in your total portfolio? TransFolio centralizes cash flows, allocations, and risks — no more separate Excel sheets.

Mini-FAQ

Ready to see how Snowflake works?

Bonds are the silent force in your portfolio. They provide stability, cash flow, and diversification. By choosing wisely between government and corporate bonds, diversifying maturities, and consolidating everything in TransFolio, you build a portfolio that brings peace of mind and delivers returns.

This blog is for educational purposes only. It does not constitute personal investment advice.